Washer & Dryer 0% Interest Financing: A Practical Guide

Discover how 0% interest financing works for washer and dryer purchases, what to watch for, and strategies to maximize savings while avoiding traps. Learn with Easy DryVent's expert guidance.

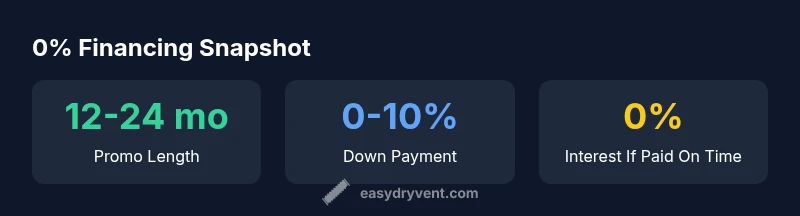

Washer dryer 0% interest financing means promotional financing that offers no interest for a set period if you pay in full before the promo ends. It can lower upfront costs and simplify budgeting for a new laundry pair. However, watch for deferred-interest traps and penalties if you miss payments or fail to pay off the balance within the promo window.

Understanding 0% APR Financing for Washers and Dryers

0% APR financing is a promotional offer where the buyer pays no interest on the purchase for a set promo period, typically tied to a retailer or manufacturer credit plan. When you purchase a washer and dryer together under a single promotion, you can manage cash flow and budgeting more predictably. However, the absence of interest only applies if you strictly adhere to the terms. If you miss a payment or fail to pay off the balance before the promo ends, interest can accrue retroactively on the entire balance or on remaining balances. Many programs require that you make minimum monthly payments or finance the entire amount through the promo. Always read the fine print, know the promo window, and confirm there are no deferred-interest clauses that would negate the savings.

Key ideas to keep in mind:

- Promo terms vary by retailer; some require you to finance the entire purchase.

- Some programs restrict eligibility to certain credit tiers or account types.

- Always verify whether the promo resets if you trade in an old unit or add accessories.

How to Qualify for 0% Financing

Qualifying for 0% financing typically hinges on a mix of credit status and retailer-specific promo criteria. You’ll often need a good credit score, a clean payment history, and an application that aligns with the lender’s terms. Many offers allow pre-qualification without affecting your credit score, which is a smart first step. Be prepared to provide standard documentation (identification, income, residence) and to accept terms like minimum monthly payments, purchase thresholds, or exclusions on certain models. If you’re shopping during a busy sale, prioritize offers that require minimal upfront costs and verify the exact promo window.

Practical tips:

- Check if the promo is tied to a particular model line or bundle.

- See whether accessories or extended warranties affect eligibility.

- Consider combining promos with price-match policies when available.

True Costs: What 0% Financing Really Means

A 0% financing offer can be appealing, but the true cost depends on how you handle the promo. If you pay the balance in full within the promo period, you avoid interest and may achieve predictable monthly payments. If you don’t, some programs convert to a standard APR for the entire balance or retroactively charge interest on the promotional period, which can dramatically raise the total cost. Always calculate the risk of late payments, administrative fees, and whether there are minimum purchase requirements that could force you into more expensive bundles. In some cases, financing with no interest can still come with other costs, like processing fees or mandatory extended warranties.

What to review before signing:

- Exact promo end date and grace period (if any).

- Whether balance transfers or combination purchases trigger different terms.

- Potential penalties for late payments or missed payments.

Retailer vs Manufacturer vs Credit Card Offers

0% financing comes from several sources, each with distinct advantages and caveats. Retailer promotions may apply to a specific brand or retailer, often bundled with installation or delivery credits. Manufacturer financing can offer deep promotions on popular models but may require installation services or fitting, while some credit cards provide intro 0% APR on purchases with different post-promo rates. The key is to compare the total cost across sources, including any fees, payment timing, and the potential for automatic conversion to a higher rate after the promo ends.

Comparison checkpoints:

- Promo length and end conditions.

- Post-promo APR and any penalties.

- Required minimums or bundles that affect total cost.

How to Compare Offers: A Quick Checklist

Use this practical checklist to compare 0% financing offers side by side:

- Confirm the promo duration and the payoff deadline.

- Determine if there is a deferred-interest clause that could retroactively apply.

- Compare required down payment, monthly payments, and any fees.

- Verify model eligibility and whether installation or delivery costs are included.

- Read the terms about what happens if you miss a payment.

Practical Shopping Scenarios: When 0% Financing Makes Sense

0% financing can be a smart choice when you have predictable income, can pay within the promo, and want to spread the cost of a new washer and dryer without paying interest. It’s particularly useful if you’re upgrading to more efficient units to save on energy costs or if you’re coordinating a home remodel. However, in situations where you cannot comfortably pay within the promo window, or where the fine print is opaque, alternative financing options could be more predictable in the long run.

Scenario insights:

- If you’re buying a bundled pair, compare the combined promo terms.

- If you’re replacing a unit with a promo tied to installation, factor in service commitments.

- If a 0% offer is available only for a short window, plan your purchase around the promo deadline.

Strategies to Maximize Savings Beyond 0% Financing

To maximize savings, combine 0% financing with price protection, delivery credits, and energy-efficiency rebates. Shop during seasonal sales, and leverage price-match policies to secure the best base price before the promo starts. Consider purchasing extended warranties only if you truly need them and if they’re not required to maintain financing eligibility. Finally, prepare a payment plan that ensures you can clear the balance before the promo ends.

Action steps:

- Set a payment calendar with reminders well before the promo ends.

- Align purchase timing with major sales events.

- Calculate total ownership costs, not just monthly payments.

Easy DryVent’s Guide: Evaluating Financing Options

From the homeowner’s perspective, evaluating 0% financing is about clarity and risk management. Easy DryVent recommends a three-step approach: (1) identify all viable offers, (2) compare the promo terms and post-promo costs, and (3) ensure you can pay within the promo window without compromising essential household expenses. We emphasize avoiding deferred-interest traps and prioritizing offers with transparent terms and minimal additional fees.

Expert takeaway: Look for offers with clearly stated end dates and no retroactive interest. Easy DryVent’s guidance is to keep the total cost in sight, not just the monthly payment.

Step-by-Step Plan for Your Next Laundry Purchase

- List your needs and preferred models; 2) gather all 0% financing offers from retailers, manufacturers, and cards; 3) compare promo lengths, fees, and post-promo rates; 4) pre-qualify to minimize hard inquiries; 5) schedule delivery and installation to align with promo dates; 6) set reminders to pay off balance before promo ends; 7) review the receipt and warranty terms after purchase.

Comparison of 0% financing options for washers and dryers

| Financing Type | Typical Eligibility | What it Covers | Risks |

|---|---|---|---|

| 0% APR Promotions | Good credit and promo eligibility | No interest during the promo term | Deferred interest or retroactive interest if not paid in full |

| Deferred-Interest Plans | Broad eligibility sometimes with store credit | Interest accrues on purchase date if terms aren’t met | Balance can grow quickly if payments slip |

| Credit Card Offers with 0% APR | Solid credit or promo approval | 0% APR during intro period on purchases | Post-promo rate can be high; plan for payoff |

Common Questions

What does 0% interest financing mean for washers and dryers?

0% financing means you won’t pay interest during the promotional period if you meet all terms. The catch is that if you miss payments or don’t pay off the balance before the promo ends, interest can accrue on the entire balance or retroactively. Always read the terms.

0% financing means no interest during the promo, but you must pay on time and pay off within the period.

Are there hidden costs with 0% financing?

Yes. Some offers include deferred-interest clauses, late fees, or require financing the entire purchase through a specific plan. Always read the terms for penalties and any required minimum payments.

Yes—watch for hidden charges like deferred interest and late fees.

Can someone with average credit qualify for 0% financing?

Many offers require at least fair credit or specific retailer eligibility, though some promotions are more broadly accessible. Pre-qualification may be available without affecting your credit score.

You can qualify, but it depends on the offer; check pre-qualification options.

How do I compare 0% financing offers?

Look at promo length, balance requirements, whether interest accrues after the promo, and total cost after any fees or down payments. Also consider installation and delivery terms.

Compare promo length, penalties, and total cost across offers.

Does 0% financing affect warranty or service?

Financing terms generally do not affect warranty or service terms, but verify with the retailer whether any financing-specific requirements apply.

Financing usually doesn’t affect warranty, but check the merchant's terms.

“"0% financing can be a smart way to manage upfront costs, but it is not magic; you must plan to pay within the promo period and read the fine print."”

Key Points

- Compare promo terms across retailers before buying

- Read the fine print to spot deferred-interest clauses

- Plan to pay off the balance within the promo window

- Consider total ownership cost, not just monthly payments